Rule 780-X-AB-.01

Ala. Admin. Code r. 780-X-AB-.01

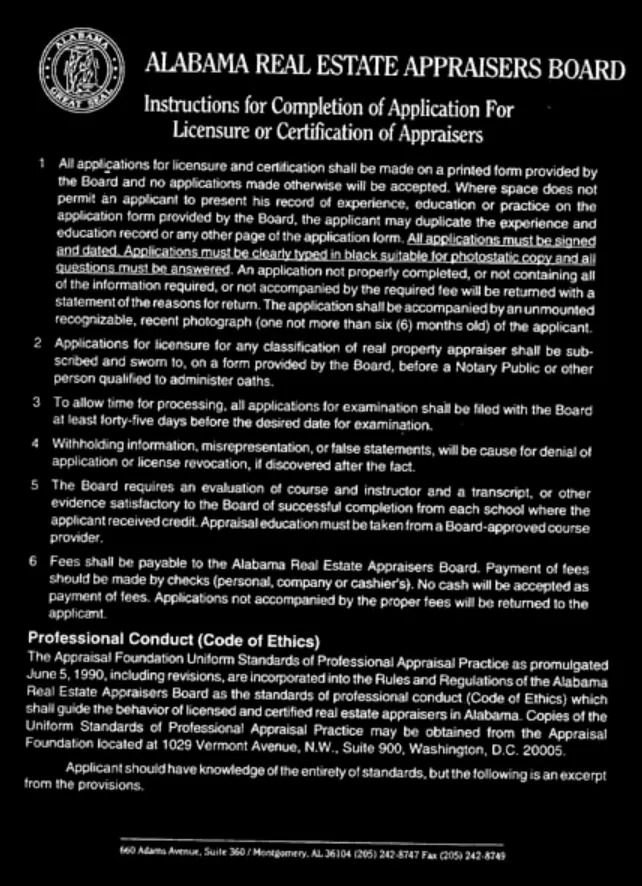

Appraisers Application Packet

Alabama Real Estate Appraisers Board

Form a11916

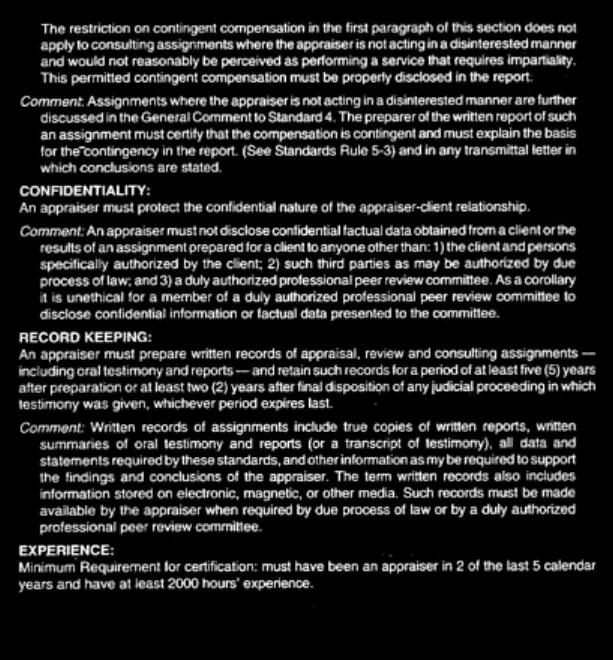

CONDUCT:

An appraiser must perform ethically and competently in accordance with these standards and not engage in conduct that is unlawful, unethical, or improper. An appraiser who could reasonably be perceived to act as a disinterested third party in rendering an unbiased appraisal, review, or consulting service must perform assignments with impartiality, objectivity, and independence and without accommodation of personal interest.

Comment: An appraiser is required to avoid any action that could be considered misleading or fraudulent.

In particular, it is unethical for an appraiser to use or communicate a misleading or fraudulent report or to knowingly permit an employee or other person to communicate a misleading or fraudulent report.

The development of an appraisal review, or consulting service based on a hypothetical condition is unethical unless: 1) the use of hypothesis is clearly disclosed, 2) the assumption of the hypothetical condition is clearly required for legal purposes, for purposes of reasonable analysis, or for purposes of comparison and would not be misleading; and 3) the report clearly describes the rationale for this assumption, the nature of the hypothetical condition, and its effect on the result of the appraisal, review or consulting service.

Individual appraisers employed by a group or organization which conducts itself in a manner that does not conform to these standards should take steps that are appropriate under the circumstances to ensure compliance with the standards.

MANAGEMENT:

The acceptance of compensation that is contingent upon the reporting or a predetermined value or a direction in value that favors the cause of the client, the amount of the value estimate, the attainment of a stipulated result, or the occurrence of a subsequent event is unethical.

The payment of undisclosed fees, commissions, or things of value in connection with the procurement of appraisal, review or consulting assignment is unethical.

Comment: Disclosure of fees, commissions, or things of value connected to the procurement of an assignment should appear in the certification of a written report and in any transmittal letter in which conclusions are stated. In groups or organizations engaged in appraisal practice, intra-company payments to employees for business development are not considered to be unethical. Competency, rather than financial incentives, should be the primary basis for awarding an assignment.

Advertising for or soliciting appraisal assignments in a manner which is false, misleading or exaggerated is unethical.

Comment: In groups or organizations engaged in appraisal practice, decisions concerning finder or referral fees, contingent compensation, and advertising may not be the responsibility of an individual appraiser, but for a particular assignment, it is the responsibility of the individual appraiser to ascertain that there has been no breach of ethics, that the appraisal is prepared in accordance with these standards, and that the report can be properly certified as required by Standards Rules 2-3, 3-2, 5-3, 8-3 or 10-3.

Form a11917